A hundred dollars is enough. That's the news, and it's genuinely news, because for most of investing history it wasn't: minimums, fees, and whole-share prices kept small money on the sidelines, and 2026's reality, fee-free brokerages, fractional shares, and index funds you can buy by the dollar, has quietly deleted every one of those barriers. The gate is open. What $100 can't buy is a shortcut, and this article won't pretend otherwise.

Here's what it will do: the two-minute pre-check that decides whether investing is even the right move for this particular $100; the actual mechanics, account, and purchase done inside an afternoon; the honest math of what small money becomes and why the habit it starts is worth far more than the money itself; and the traps aisle, which preys on small accounts specifically. The standing line, as always, is our money Articles: General information, not financial advice. Products and tax rules differ across the US, UK, Canada, and the Gulf, and your decisions deserve your own research or a professional's eye.

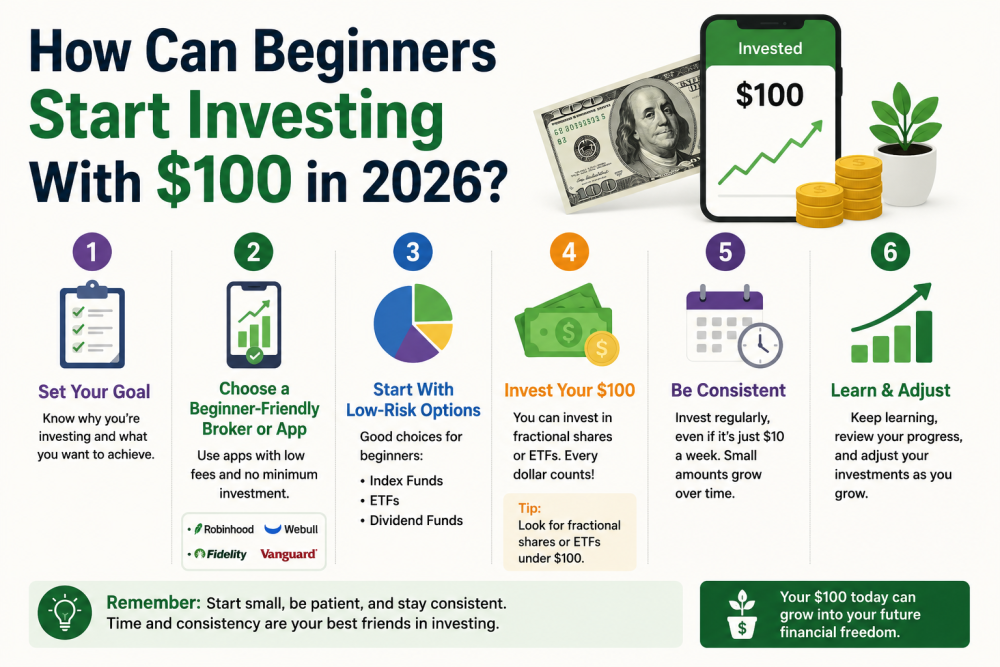

The Pre-Check: Is This $100 Actually for Investing?

Sixty seconds of honesty before any account gets opened, running the order of operations our finance guides share. If you're carrying high-interest debt, a 20-something percent card, this $100 earns its best guaranteed return paying that down; nothing on any market reliably beats it. If there's no starter emergency buffer at all, this $100 might be the beginning of one in a high-yield savings account because investing without any cushion means selling at the worst moment when life happens; the whole case is in our emergency fund guide. And if this money has a date attached, needed within a couple of years, it belongs in savings, not markets, per the sort-by-date rule our safest investments article runs on.

Passed all three? Then this $100 is genuinely investable: money with no job and no deadline, which is exactly the kind that belongs in markets. Proceed.

The Mechanics: Account, Purchase, Done

Step one, the account. You want a regulated brokerage in your country with three features that all became standard in 2026: no account fees or commissions on basic trades, fractional investing, buying by the dollar amount rather than the share, and no minimum deposit. Most major brokerages and the reputable investing apps in each of our reader countries now tick all three; ten minutes of comparison on those criteria, plus confirming local regulation, beats any specific name an article could date itself with. Where your country offers a tax-advantaged wrapper, a retirement account in the US, an ISA in the UK, a TFSA in Canada, opening the brokerage account inside one is the free upgrade almost every beginner skips, and it's worth the extra form.

Step two is the purchase, and it's one purchase: a broad, low-cost index fund, the whole-market kind our beginners' investing guide explains in depth, one buy, hundreds or thousands of companies, fees near zero, and no picking required. With fractional investing, your $100 buys $100 of it, decimal points included, and the transaction takes less time than reading this paragraph. That's it. That's investing. The industry's complexity is mostly upsells.

The Honest Math, and What $100 Actually Buys

Now the part that keeps this article honest. One hundred dollars, left alone for thirty years at the long-run-ish illustrative rate of about 7 percent annually, becomes roughly $760; it's pleasant, not life-changing, and anyone selling you a different story about a single small deposit is selling. Small money's compounding is real and slow, and pretending otherwise is how beginners end up disappointed or gambling.

Here's what changes the math entirely: repetition. The same $100 start, plus a modest automatic amount weekly or monthly, and the automation habit from our savings guides pointed at the brokerage instead, compounds over decades into the six-figure territory that actually changes lives, and every calculator on the internet will happily show you your version of that curve. Which reveals what the first $100 truly buys, and it's not the $760: it's the machine, installed. The account that exists, the automatic transfer that runs, and the market swings experienced early on make money small enough that the lessons are cheap, watching your $100 become $92 in a bad month and learning, viscerally, that you don't sell and that education costs universities money when learned at $10,000 and costs eight dollars when learned at $100.

The first hundred is tuition and infrastructure. The wealth comes from the habit it starts, which is why starting with "only" $100 isn't the compromise version of investing. It's the correct entry, at the safest possible scale.

The Traps Aisle: Built for Small Accounts

Small money attracts specific predators, so the tour. The single-stock lottery: putting $100 on one exciting company isn't investing; it's a scratch card with a ticker symbol, and the index fund exists so you never need to be right about individual companies. The crypto moonshot pitch, "turn $100 into $10,000," is the same lottery with worse odds and better marketing; our Bitcoin guide's framing stands: anything crypto is speculation with money you can afford to lose, never the foundation. Fees, the quiet killer at this scale: a $2 monthly account fee is 24 percent of a $100 portfolio annually, which is why the no-fee criterion above isn't preference; it's arithmetic. Day trading apps' confetti and streak mechanics: engagement design pointed at your principal. And the courses: $200 investing courses sold to $100 investors, costing double the portfolio to teach what this article and the free resources in every direction cover, the reliable rule from our money guides, anything urgent, guaranteed, or exclusive is priced on hope.

The pattern: everything in the traps aisle offers speed. Everything that works offers repetition. Small accounts can't afford speed's failure rate, and happily, they're the perfect size for repetition.

Scaling: From $100 to an Actual Portfolio

The staircase after the start, briefly, because the fuller versions live across our finance cluster. Automate the addition of any amount; $10 a week counts, on payday, per the pay-yourself-first mechanics in the savings guide, and let the amount grow as income does, including raises, side hustle money, and the windfall rule's fixed slice. Stay boring: the same broad fund, bought automatically, is ignored heroically. Checking daily is for weather, not portfolios. Use the tax wrapper if you skipped it at setup. And revisit the bigger map as the numbers grow, the emergency fund is completed, the sort-by-date buckets are filled, and the whole architecture in our beginners' guide is updated, because a $100 start has a way of becoming a real portfolio faster than the honest math suggests, not through returns but through the habit of quietly raising the deposits.

The Bottom Line

Starting to invest with $100 in 2026: run the pre-check; expensive debt and a starter buffer outrank markets; open a no-fee, fractional, regulated brokerage account inside your country's tax wrapper if one exists; buy $100 of a broad, low-cost index fund; and install the automatic addition that turns the gesture into the machine. Expect the money itself to compound slowly and honestly; expect the habit to be the actual asset; and walk past the entire traps aisle, the single-stock lotteries, the moonshots, the fees, and the courses that exist precisely because small accounts outnumber large ones.

A hundred dollars won't make you wealthy. The investor it makes you, started early, educated cheaply, automated permanently, very well might, and 2026 is the first era where that entry costs nothing extra. The gate's open. Walk through it boringly and keep walking.

FAQs: Investing With $100

Is $100 really enough to start investing in 2026?

Yes, genuinely: fee-free brokerages, no minimums, and fractional shares mean $100 buys a diversified slice of the whole market in one purchase. What it can't do is compound into wealth alone; its real value is starting the account, the automation habit, and the cheap early education that make the later, larger investing work.

What should a beginner buy with their first $100?

One thing: a broad, low-cost index fund, the whole-market kind, bought fractionally, which delivers instant diversification across hundreds of companies with near-zero fees and no stock-picking required. It's the standard beginner recommendation across the credible investing world, and our beginners' investing guide covers the reasoning in full.

How much will $100 grow if I invest it?

Honest illustration: at a long-run style 7 percent annually, $100 alone becomes roughly $200 in a decade and around $760 in thirty years, real, modest, and slow. The transformation comes from additions: the same start plus small automatic weekly or monthly contributions compound into genuinely life-changing figures over decades, which is why the habit, not the hundred, is the asset.

Should I invest $100 in stocks or crypto instead?

A single stock turns your $100 into a bet on one company's fate, and crypto's defining volatility makes it speculation rather than a foundation. Our Bitcoin guide's rule applies: only ever money you can afford to lose, on top of boring foundations, never instead of them. The index fund route wins for the first $100 precisely because it requires being right about nothing.

What fees should I watch out for with a small account?

Percentage arithmetic is brutal at this scale: a $2 monthly fee consumes 24 percent of a $100 portfolio in a year, so the account must be genuinely free of maintenance fees and commissions, and the fund's expense ratio should sit near the low-cost index standard. The no-fee criterion isn't a preference for small investors; it's survival.

Is it better to save or invest my first $100?

Run the order: high-interest debt gets paid first (a guaranteed return nothing matches), a starter emergency buffer in savings comes next (so surprises don't force selling), and money needed within a couple of years stays in a high-yield savings account regardless. The first $100 with no debt behind it, no job, and no deadline is the one that belongs in the market, and that's the pre-check in sixty seconds.