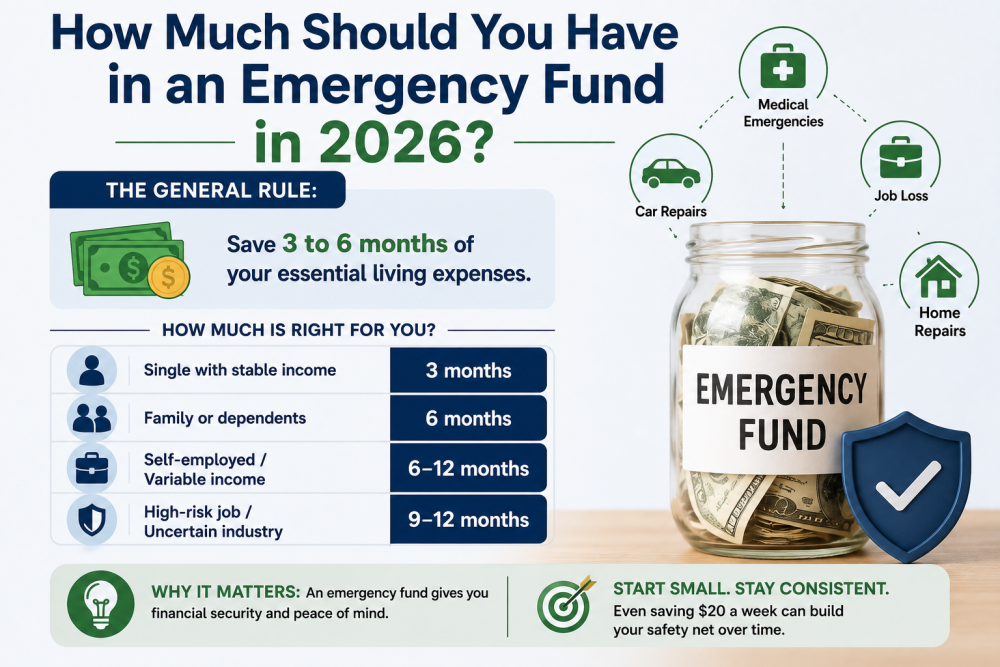

Three to six months of essential expenses. That's the standard answer, it's still the right neighborhood in 2026, and it's also nearly useless until two words in it get defined properly, because "essential" and "expenses" are where everyone's number goes wrong.

So this article does the definition work: what actually counts in the monthly figure, and it's smaller than your lifestyle, who genuinely needs six months or more and who's fine nearer three, the starter-fund stage that comes before any of it, where the money should physically sit, and the question people are embarrassed to ask, what officially counts as an emergency once the fund exists. Boring topic, arguably the most load-bearing number in personal finance, let's get it right.

Standing disclaimer, plain voice: general information, not personal advice, circumstances and safety nets differ across the US, UK, Canada, and the Gulf, and big financial decisions deserve a professional who knows your specifics.

Step One: The Number Underneath the Number

Your emergency fund multiplies a monthly figure, so the monthly figure comes first, and here's the correction that shrinks most people's mountain: it's essential expenses, not income, and not your current lifestyle.

Sit down once and total the survival month: housing, utilities, groceries (groceries, not restaurants), transport, insurance, minimum debt payments, phone, essential family and medical costs. Not subscriptions-plural, not travel, not the discretionary layer, in a real emergency those pause, which is the point. For most people this survival number lands meaningfully below their normal monthly spend, often 60 to 70 percent of it, which means the fund target just dropped by a third before you saved a unit of currency. A six-month fund is six months of that number, not six months of your salary, and the difference is the difference between a mountain and a hill.

Step Two: Three Months, Six, or More? The Honest Sort

The range exists because risk differs, and sorting yourself takes one honest look at two things: how stable the income is, and how many incomes there are.

Closer to three months works when income is genuinely stable and redundant: dual-earner households where both jobs are secure, salaried roles in steady industries, strong family or state safety nets underneath. One income stumbles, the other holds the line while you fix it.

Six months is the sensible default for the single-income household, the salaried-but-in-a-volatile-industry, homeowners (houses invent emergencies), and parents, dependents multiply the ways a month can go sideways.

More than six, up to nine or twelve, earns its keep for exactly the readers our side hustle and freelancing guides serve: variable-income workers, freelancers, commission earners, small business owners, and anyone whose income and emergencies can arrive holding hands, the client who vanishes is often the same event as the income gap. Irregular income doesn't just need a bigger buffer, it needs the buffer doing double duty as a salary-smoother, and the freelancers who sleep well are almost universally the ones carrying fat funds.

One more honest modifier for 2026: job searches in many white-collar fields have been running longer than the old rules assumed, and the fund's real job is outlasting your realistic re-employment time. If people in your role and market take six months to land well, a three-month fund is a plan to panic in month two.

Step Three: The Starter Fund Comes First, Always

Before the months-of-expenses project, the small fund, and this sequencing matters enough that our debt and savings guides both hammer it: get a starter buffer of roughly $500 to $1,000, or about one month of essentials, in place before aggressive debt payoff or anything else ambitious.

The mechanism, once more, because it's the whole argument: without any buffer, the first surprise, the car, the tooth, the boiler, goes straight onto a card at brutal interest, and the cycle you're fighting refinances itself. The starter fund isn't the emergency fund. It's the thing that stops emergencies from compounding while you build the real one, and for readers carrying expensive debt, the order is exactly this: starter fund, then the debt, then the full fund, the math and the psychology both bless that sequence.

Where the Money Lives, and Where It Doesn't

The emergency fund has one job, being there, instantly, in full, on the worst day, and every location decision follows from that.

It lives in a high-yield savings account, deposit-insured, ideally at a different bank from your daily spending, the separation adds just enough friction to stop casual raids while staying same-day accessible. In the current rate era it even earns respectably while it waits, which is new and pleasant.

It does not live in investments, and this is the mistake ambitious savers make: stocks and funds can be down 20 or 30 percent on precisely the day you need the money, and emergencies have a documented sense of humor about timing, recessions deliver job losses and market drops in the same envelope. The fund's return is measured in disasters survived, not percent. Growth money is a different bucket with a different article, our beginners' investing guide, and the two buckets should never share a wallet.

And it doesn't live in cash under anything, inflation and burglars agree on that one, or locked in fixed terms that penalize the exact withdrawal the fund exists for.

Building It Without Hating Your Life

The full fund takes most people one to three years, and that's fine, it's infrastructure, not a sprint. The build runs on the machinery our low-income savings guide details: an automatic transfer on payday, sized to survive bad months, plus the windfall rule, a fixed slice of tax refunds, bonuses, and gift money going straight in, windfalls are where funds actually get fat. Milestones keep morale: one month banked changes your sleep, three months changes your posture at work, six changes your relationship with risk entirely, and each one is worth marking.

Then the two rules of the finished fund. What counts as an emergency: unexpected, necessary, urgent, all three, the job loss, the medical bill, the dead car you need for work. Not the sale, not the wedding, not the predictable annual expenses, those get their own small "sinking funds" saved monthly, insurance renewals and holidays are appointments, not ambushes. And after any withdrawal, replenishment becomes the top savings priority again, using it was the system working, refilling it is the system continuing.

The Bottom Line

The 2026 answer, properly defined: three to six months of essential expenses, the survival month, not the lifestyle month, sorted honestly by your income stability, three-ish for dual stable incomes, six as the default, more for freelancers, single earners, and anyone whose job market moves slowly. Before it, the $500-to-$1,000 starter fund that breaks the borrowing cycle. Around it, insured savings at arm's length from daily spending, never investments. Behind it, automation, windfalls, and the patience of a one-to-three-year build.

It's the least exciting money you'll ever accumulate, and it buys the most expensive thing on sale anywhere: the ability to have a bad month without having a bad year. Price the fund against that, and the months of saving start looking cheap.

FAQs: Emergency Funds in 2026

Is $1,000 enough for an emergency fund?

As the starter stage, yes, roughly $500 to $1,000, or one month of essentials, is exactly the right first target, and it comes before aggressive debt payoff because it breaks the surprise-expense-to-credit-card cycle. As the finished fund, no: the full target is three to six months of essential expenses, built after expensive debt dies.

Should my emergency fund be 3 or 6 months?

Sort by income stability: closer to three months suits dual stable incomes and secure salaried roles; six is the honest default for single-income households, parents, and homeowners; and freelancers, commission earners, and business owners genuinely need six to twelve, since their emergencies and income gaps often arrive together. Add months if job searches in your field realistically run long.

Where should I keep my emergency fund in 2026?

In a deposit-insured high-yield savings account, ideally at a different bank from your spending account, instantly accessible, earning decent interest, and separated enough to discourage casual raids. Not in investments, which can be deeply down on exactly the day you need them, and not locked in fixed terms that penalize the withdrawal the fund exists for.

Should I build my emergency fund or pay off debt first?

The sequence that works: starter fund first ($500 to $1,000), then high-interest debt, then the full three-to-six-month fund. The starter buffer exists so the first surprise doesn't refinance the debt you're fighting, and the full fund waits because paying off a 20-plus percent card is a guaranteed return no savings account matches, the same order our debt payoff guide walks in detail.

What counts as a real emergency?

Three tests, all required: unexpected, necessary, urgent. Job loss, medical bills, the essential car repair, the boiler in winter, yes. Sales, holidays, weddings, and annual insurance renewals, no, the predictable ones get their own small sinking funds saved monthly so they stop impersonating emergencies. And using the fund for a genuine emergency isn't failure; that's the machine doing its one job.

How do I calculate my emergency fund amount?

Total one survival month, housing, utilities, groceries, transport, insurance, minimum debt payments, phone, essential family and medical costs, excluding the discretionary layer that pauses in a crisis. That figure usually runs well below normal monthly spending. Multiply by your months from the stability sort above, and that's the target: personal, honest, and almost always smaller than the salary-based number that scared you off starting.