When the Federal Reserve 2026 Rate makes a decision about interest rates, people outside the US sometimes wonder why they should care. The answer is that whether you're buying a flat in London, refinancing an apartment in Frankfurt, or trying to get onto the property ladder in Sydney, the Fed's choices ripple outward in ways that are real, measurable, and—for anyone with a mortgage or hoping to get one—genuinely worth understanding.

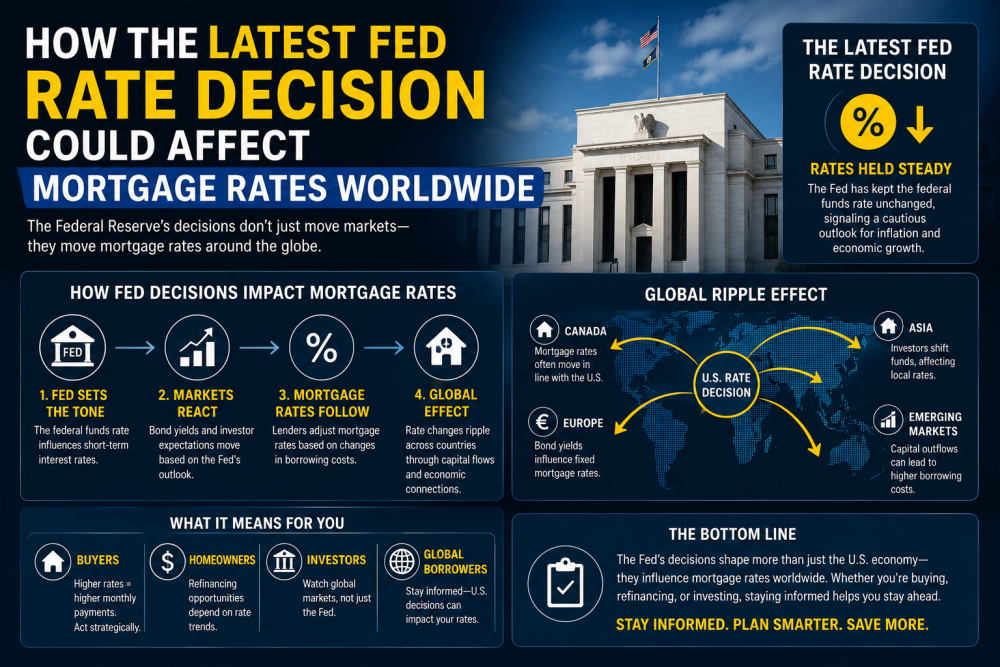

On June 17, 2026, the Federal Open Market Committee voted unanimously—12 to 0—to hold the federal funds rate steady at its current range of 3.50% to 3.75%. On the surface, that sounds like a non-event. Nothing moved, right? But the story underneath that hold is considerably more complicated, and for mortgage borrowers around the world, the implications aren't what most people expected going into the year.

What Actually Happened at the June Meeting

The hold itself was no surprise. Markets had fully priced it in. What did catch people off guard was the tone that came with it—and the projections the Fed released alongside the decision.

The updated "dot plot"—a chart where each Fed official marks where they expect rates to be at year-end—shifted meaningfully toward a hike. Of the 18 officials who submitted a forecast, nine now see rates rising before 2026 is out. The median projection for end-2026 moved up to 3.8%, compared to 3.4% in March. That's not a small shift. It means the Fed has gone from leaning toward cuts to leaning toward another hike, all within a few months.

The new Fed Chair, Kevin Warsh, presided over this meeting for the first time after being sworn in on May 22. His press conference was notably blunt—he acknowledged inflation remains well above the 2% target (it hit 4.2% in May, the highest since 2023), and he signaled the Committee's cutting bias has been removed from its policy statement. He also declined to submit his own dot plot projection and announced task forces to overhaul how the Fed communicates policy going forward.

Markets responded accordingly. Treasury yields rose, stocks fell, and traders moved to price in a rate hike as soon as October 2026.

That context is everything when you're trying to understand what this means for mortgage rates.

Why the Fed Rate Isn't the Same as Your Mortgage Rate

This is the part that confuses a lot of people, and honestly it's worth clearing up because the relationship is indirect.

The federal funds rate is the overnight rate banks charge each other for short-term loans. Mortgage rates—particularly the 30-year fixed-rate mortgage that most US homeowners use—are much more closely tied to the yield on 10-year US Treasury bonds. Those yields reflect what the bond market collectively thinks about future inflation, economic growth, and yes, what the Fed is likely to do down the road.

So when the Fed holds but signals more tightening ahead, the bond market doesn't shrug. It reprices. Yields move higher. And mortgage rates follow.

That's exactly what's been happening. The 30-year fixed mortgage rate currently sits around 6.53% as of late June 2026, having climbed back up from a low of around 6.09% earlier in the year. Back in February, when markets were still anticipating rate cuts, rates had briefly dipped below 6%. That window closed.

The other major driver has been the Iran conflict, which started in late February and has kept oil prices elevated, feeding inflation pressures that were already sticky before geopolitical tension entered the picture. The Fed's statement explicitly cited this as a factor.

So for US borrowers: don't expect a meaningful drop in mortgage rates anytime soon. Several major housing authorities predicted rates would fall to the mid-5% range by mid-2026. That forecast is looking increasingly optimistic. Housing economists broadly now expect rates to stay above 6% through the rest of the year, and a hike later in 2026 would push them higher still.

The Squeeze on US Homebuyers

The numbers on affordability are worth sitting with for a moment, because they're stark.

The median existing home price in May 2026 was $429,300—an all-time high for the month. The national median family income is around $106,800. With a 20% down payment and today's mortgage rate of roughly 6.5%, the monthly principal and interest payment comes to about $2,166, which represents roughly 24% of the typical family's monthly income.

That's not catastrophic—traditional guidelines say housing costs under 28% of income is manageable—but it's tight. And it's worth remembering that 20% down on a $429,000 home is nearly $86,000, an amount most first-time buyers don't have sitting around.

Think about what this means practically. A couple in their early 30s who started saving for a down payment in 2023 may have been told to expect mortgage rates of 5-something percent when they were finally ready to buy. They've done everything right—saved diligently, improved their credit—and the environment they're stepping into looks nothing like what they planned for. That's the frustration underlying a lot of the conversations happening around kitchen tables right now.

The one silver lining: home price growth is slowing significantly. More than half of the 20 major US housing markets recorded year-over-year price declines as of March 2026, according to the S&P Cotality Case-Shiller index—the weakest showing since 2011. So supply-demand dynamics may eventually help, even if rate relief doesn't arrive quickly.

How This Spreads Globally

Here's where the Fed's influence becomes something bigger than a domestic US story.

The US dollar is the world's reserve currency. US Treasury bonds are the benchmark against which virtually every other sovereign debt instrument is priced. When Treasury yields rise—because bond markets are repricing to account for a Fed that's staying tighter for longer—global capital flows respond. Money moves toward higher-yielding dollar assets, which pushes other currencies weaker against the dollar, which then creates its own inflationary pressures in those countries (imports get more expensive when your currency weakens).

Central banks abroad then face a choice: accept higher domestic inflation, or defend their currencies and contain inflation by keeping their own rates elevated too.

This is the mechanism by which a Fed decision in Washington affects mortgage rates in Manchester, Melbourne, and Mumbai.

What's Happening in Europe

The European Central Bank actually moved in the same direction as the Fed—but independently, for its own reasons. At its June 11 meeting, the ECB raised its deposit rate by 25 basis points to 2.25%, citing inflation pressures from the Middle East conflict. This came after eight consecutive rate cuts between June 2024 and June 2025, making it a notable reversal.

For European homeowners with variable-rate mortgages—which are far more common in continental Europe than in the US—this is directly painful. Countries like Spain, Portugal, and parts of Italy have large numbers of mortgages tied to the Euribor (the eurozone's interbank rate), which moves closely with ECB policy. Even a quarter-point move creates real monthly payment increases for borrowers carrying existing debt.

In Germany and France, fixed-rate mortgages are more prevalent, so existing borrowers are more insulated—but anyone renewing or taking out a new loan is facing a more expensive environment than they would have seen even 12 months ago.

What's Happening in the UK

The Bank of England has been navigating a somewhat different situation. After four cuts in 2025, the BoE has been cautious about further easing, particularly with the Iran conflict adding energy-driven inflation that the UK—which imports considerable energy—feels acutely.

UK mortgage markets are heavily concentrated in shorter fixed terms—2-year and 5-year fixes—unlike the US's dominant 30-year product. This means a much larger portion of UK borrowers roll off their fixed rates within any given year and are directly exposed to current market rates. Some economists estimate that millions of UK homeowners have been or will be moving from sub-2% pandemic-era fixes to current rates in the 4-5% range over 2025-2026, representing a significant shock to monthly budgets.

The Fed's hawkish turn won't help. If US yields stay elevated, UK gilt yields tend to stay elevated too—and UK mortgage rates price off gilt yields. It's not a perfect correlation, but the direction is clear.

Australia, Canada, and Emerging Markets

Australia and Canada share something with the UK: housing markets that stretched dramatically during the low-rate era and are now experiencing the hangover. Both have large numbers of variable-rate mortgages and shorter fixed terms. Both central banks cut rates through 2025, but neither can easily cut further if the Fed is signaling a potential hike and their currencies risk weakening in response.

For emerging markets, the dynamics are more severe. Countries that carry dollar-denominated debt—common across Latin America, parts of Asia, and Africa—face higher repayment costs when the dollar strengthens. A Fed that stays hawkish keeps the dollar stronger, which squeezes governments and corporations in these economies. Property markets in these countries can feel the effects even when the local central bank isn't doing anything unusual.

India, for instance, runs a significant current account deficit and is sensitive to dollar strength. The Reserve Bank of India has to weigh domestic growth needs against currency defense when the Fed tightens—a genuine policy dilemma that plays into the broader cost of borrowing for Indian homebuyers.

What Borrowers Should Actually Do With This Information

Let's get practical, because understanding what's happening globally only helps if you can apply it to your own situation.

If you're a US homebuyer or refinancer right now: The expectation of rate cuts that many were hoping for has essentially evaporated. Waiting for a significant drop in mortgage rates is a strategy with real risk attached to it—rates could climb further if the Fed hikes in October. If you find a rate you can make work in your budget, locking it in sooner rather than later has merit. That said, don't let urgency push you into a home you can't comfortably afford. Overstretching on housing is a mistake that compounds badly if rates move against you or economic conditions shift.

If you have a variable-rate mortgage in Europe or the UK: Now is a reasonable time to pressure-test whether you could handle another 50-75 basis points of rate increases. Not because that's guaranteed, but because the direction of risk has shifted. Having that conversation with your lender or mortgage broker is a better use of energy than hoping central banks reverse course quickly.

If you're in the market to buy internationally: Currency dynamics add a layer of complexity. A stronger dollar can actually work in your favor if you're earning in USD and buying in a market where the local currency has weakened—but it cuts the other way for local buyers in those markets.

For everyone: the single most practical thing is to stress test your finances at rates somewhat higher than today's. If the numbers only work in an optimistic rate environment, that's a vulnerability worth addressing before it becomes a crisis.

The Bigger Picture

What's unusual about the current environment is that central banks worldwide reached elevated rates for similar reasons—post-pandemic inflation—but are now diverging in their paths forward based on local conditions. The ECB just hiked while other central banks are pausing. The Fed, after cutting three times in late 2025, has not only stopped cutting but is now openly signaling the next move could be upward.

This divergence creates volatility in currency markets, bond markets, and ultimately in the mortgage rates that households pay. The world got used to a decade of low rates followed by a synchronized hiking cycle. What we're in now is messier—different economies at different stages, responding to different pressures, pulling capital flows in competing directions.

For mortgage borrowers, the takeaway isn't to panic. It's to stop assuming that the favorable rate environment of 2020-2021 is coming back anytime soon. The Fed's June 2026 decision—technically a hold, functionally a hawkish signal—reinforces that message clearly.

The cost of borrowing is higher than it was, and the central bank most influential in setting the global cost of money has just told us it's not in a hurry to change that. Planning around reality, rather than waiting for a return to what once was, is the most useful thing anyone can do right now—whether they're buying a home in Phoenix, remortgaging in Bristol, or financing a flat in Frankfurt.