Let's start with the uncomfortable truth that most AI investing guides skip past: if you already hold a diversified index fund portfolio, you're already significantly exposed to AI stocks. The S&P 500's largest positions — Nvidia, Microsoft, Alphabet, Meta, Amazon — are all central AI plays. Adding individual AI names or narrowly focused AI ETFs on top of an index portfolio could mean you're concentrating risk rather than gaining access to something new.

That said, the AI investment opportunity is real, and for investors who want more direct exposure than a broad index provides, there are sensible ways to get it. The key is understanding the structure of the AI investment landscape — and being clear-eyed about the risks that the bullish headlines tend to downplay.

The Case for Staying Interested Despite the Volatility

Before getting into the how, it's worth being clear about the what.

AI startups are scaling from $1 million to $30 million in revenue five times faster than SaaS companies did. The major hyperscalers — Microsoft, Amazon, Alphabet, and Meta — are expected to collectively spend over $700 billion on AI infrastructure in 2026. Nvidia's revenue growth has been extraordinary by historical standards. CoreWeave went from minimal sales in 2022 to $5.1 billion in 2025 and is expected to generate more than $10 billion in revenue in 2026.

The flip side: many economists have warned that investors could be overvaluing AI, and many recent periods of stock market volatility — including the tech-stock-focused downturn of June 2026 — have been linked to wavering confidence in AI among investors. The dot-com comparison circulates in academic circles, though it's contested. The distinction that matters is whether current valuations are supported by real earnings — and for the largest AI companies, the revenues and profits are genuinely there in ways that were not true of dot-com era companies. For smaller, pre-profitability AI companies, the speculative element is real.

None of this says "don't invest in AI." It says "know what you're buying and why."

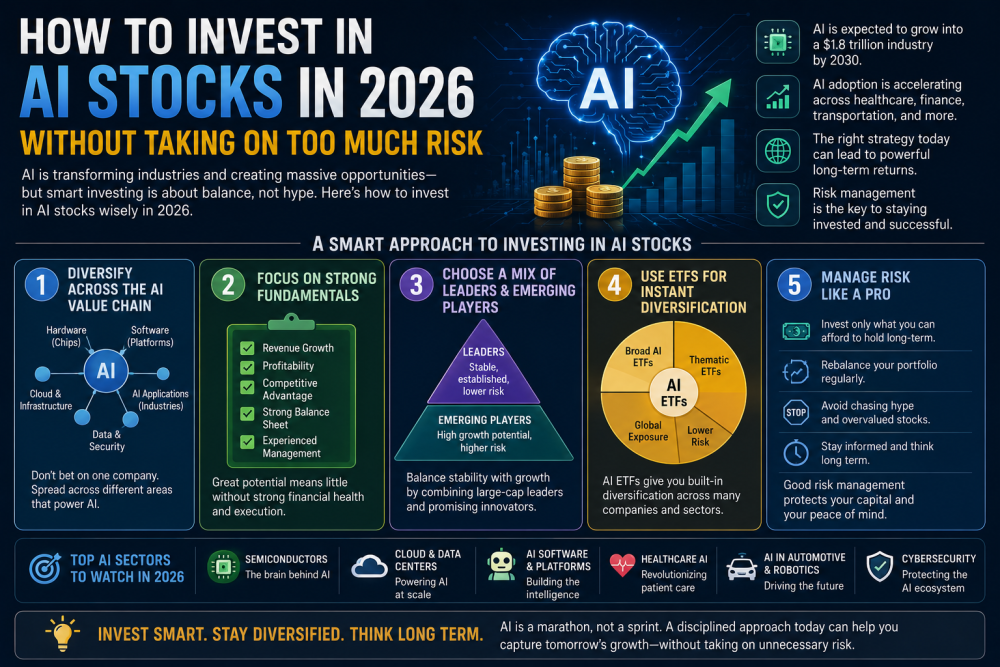

Thinking in Layers: The AI Value Chain

The most useful mental model for AI investing is the value chain — the different layers of the AI ecosystem, each with different risk profiles and return characteristics.

Layer 1: Chips and compute — This is the foundation. Nvidia dominates, with an estimated 80–90% of the AI training chip market through its H100 and Blackwell GPU architectures. AMD is the primary challenger, offering more execution risk but more upside if its roadmap lands. Broadcom supplies custom AI accelerators to hyperscalers like Google and Meta, with its AI semiconductor revenue projected to double year-over-year in 2026.

The risk at this layer is twofold: geopolitical (TSMC, which manufactures the chips, is headquartered in Taiwan, introducing concentration risk around US-China tensions) and competitive (hyperscalers are increasingly designing custom chips to reduce their dependence on Nvidia). Neither risk is a near-term crisis, but both are real.

Layer 2: Physical infrastructure — Data centres need power, cooling, and connectivity. Vertiv, which provides thermal management and power equipment for data centres, saw Q4 2025 orders climb 252% and its backlog surge 109% to $15 billion. Vertiv is one of the better AI investments not called Nvidia because it benefits regardless of which chip maker wins the GPU race. Arista Networks connects the GPU clusters that make large-scale AI possible. These companies are AI picks-and-shovels plays — they benefit from AI infrastructure spending without the direct exposure to chip competition.

Layer 3: Cloud platforms and hyperscalers — Microsoft, Alphabet, Amazon, and Meta are the large-scale operators who rent AI capacity to the world and deploy it within their own products. These companies combine massive existing cash flows with meaningful AI revenue growth. Microsoft's Azure AI services are growing faster than the core cloud business. Meta AI is embedded across Facebook, Instagram, and WhatsApp and reached 1 billion monthly active users in 2025.

At this layer, the risk for megacaps like Alphabet and Meta is cyclical advertising dependence — when the economy softens, ad revenue contracts. But in the long run, AI improvements are expected to drive significant growth in their core ad businesses.

Layer 4: Software and platforms — This is where AI turns into enterprise revenue. Palantir delivered 70% year-over-year revenue growth in Q4 2025, with US commercial revenue surging 137%. ServiceNow's Now Assist product crossed $600 million in annual contract value and is on track to reach $1 billion by end of 2026. Adobe's Creative Cloud now features AI tools deeply integrated into workflows. These application-layer companies face the highest valuation risk — the business can compound well while the stock still falls if growth merely slows from elevated expectations.

The Four Risks Worth Understanding

Most AI investing commentary focuses on the upside. Here are the four risks that are genuinely worth sitting with:

1. Capex fatigue — The entire AI supply chain rests on the assumption that hyperscalers (Microsoft, Amazon, Alphabet, Meta) will continue spending aggressively on AI infrastructure. If even one major buyer guides that spending down, investors will reprice the whole supply chain within hours. Watch hyperscaler capex guidance in quarterly earnings closely — it's the single most important indicator for the AI hardware supply chain.

2. Monetisation lag — AI tools are improving fast, but revenue has to grow faster than the depreciation and power costs of the hardware behind them. The question of whether and when AI tools will generate returns that justify $700 billion in annual infrastructure spending is genuinely open. Some companies (Microsoft's Copilot, Google's advertising AI, Meta's ad targeting) are already showing returns. Others are still in the "we're investing for the future" phase, which is a less comfortable place for investors who paid premium valuations.

3. Valuation sensitivity — Application-layer AI companies trade at multiples that price in extended high-growth scenarios. Palantir, for example, carries significant execution risk where even successful business performance doesn't necessarily produce stock returns if growth decelerates from elevated expectations. These are high-conviction, high-volatility holdings, not conservative positions.

4. Geopolitical disruption — Export controls on semiconductor technology, US-China tensions affecting Taiwan and TSMC, and shifting regulations in different jurisdictions all create tail risks for AI stocks. Nvidia's export controls on China sales are an ongoing issue. Any escalation in Taiwan Strait tensions would immediately impact the chip supply chain in ways that would ripple across the entire AI investment universe.

Three Ways to Build AI Exposure Without Overconcentrating

Option 1: Let your index funds do the work (the conservative approach)

If you're primarily an index investor, you already own significant AI exposure. The five largest positions in the S&P 500 index — Nvidia, Microsoft, Alphabet, Amazon, Meta — represent substantial AI weight in any broad US equity index fund. Before adding anything, check how much you already have. Many people who think they have no AI exposure actually have substantial indirect exposure through these positions.

Option 2: AI ETFs for thematic exposure with diversification

If you want more direct AI exposure than a broad index provides, AI-focused ETFs are the most straightforward way to get it without single-stock risk. Popular examples include the Global X Artificial Intelligence & Technology ETF (AIQ), the iShares Exponential Technologies ETF (XT), and the ARK Autonomous Technology & Robotics ETF (ARKQ). BlackRock also maintains the iShares A.I. Innovation and Tech Active ETF (BAI) for those who want an actively managed option.

ETFs reduce single-stock risk but come with expense ratios and may hold companies with varying degrees of genuine AI exposure. Some AI ETFs hold companies that have AI in their name but limited real AI business. Read the holdings before you buy. The best ETFs for AI exposure are generally those focused on the infrastructure and enablement layers (semiconductors, data infrastructure) rather than broad "AI theme" products that can include companies with marginal AI involvement.

Option 3: A layered individual stock approach (for active investors)

Building a balanced AI portfolio means investing across four layers of the value chain. Chips and compute: NVIDIA remains the leader and your core AI holding. Networking: Arista Networks connects the GPU clusters that make AI possible. Physical infrastructure: Vertiv powers and cools the data centres running AI workloads. Software and platforms: Palantir and ServiceNow monetize AI at the application layer.

This layered approach reduces concentration risk considerably. If Nvidia faces a competitive challenge from AMD or custom hyperscaler chips, your Arista and Vertiv positions are largely insulated. If application-layer software valuations compress, your infrastructure positions continue benefiting from underlying capex spending.

A common portfolio structure that many active investors use: a core position in one or two megacap names (Microsoft, Nvidia, Alphabet), supplemented by infrastructure plays (Arista, Vertiv, Broadcom), with a smaller allocation to application-layer companies sized according to individual risk tolerance.

The IPO Situation: OpenAI and Anthropic

One of the most-watched developments in AI investing for the remainder of 2026 is the potential public offering of the two most prominent frontier AI labs. Both OpenAI and Anthropic confidentially filed S-1 forms with the Securities and Exchange Commission in June 2026, indicating they're planning to go public, with some reports suggesting both could start trading before the end of the year. Both companies were valued near $1 trillion after their most recent respective rounds of fundraising.

If retail investors are allowed to participate directly in these IPOs, they'll need to act through brokers that offer IPO access — these aren't typically available on all platforms. For those who want indirect exposure before or regardless of the IPOs, Anthropic's partnership with Amazon (AWS) and OpenAI's partnership with Microsoft already provide partial indirect exposure through those publicly traded companies.

Whether investing in these IPOs at the expected valuations makes sense depends entirely on price at offering. High-growth companies can be excellent businesses and poor investments if the entry price already reflects years of expected growth. Watch the filing disclosures carefully when they become public — the revenue numbers, growth rate, and path to profitability will tell you whether the valuation is supportable.

Portfolio Sizing: The Practical Question

The honest answer to "how much of my portfolio should be in AI stocks" depends entirely on your situation — time horizon, other holdings, risk tolerance, and whether you're already indexed. But a few principles apply broadly:

AI as a theme is not a diversified position. Owning five AI stocks is more concentrated, not less, than owning one broad index fund that includes Nvidia, Microsoft, and Alphabet in large weights. If you're adding AI stocks on top of an index portfolio, recognise that you're increasing your effective technology concentration, not broadening your portfolio.

Position sizing in higher-risk names should reflect their volatility. A 10% portfolio position in Palantir or CoreWeave creates meaningful drawdown risk if those positions move against you. A 2–3% position in a high-conviction but higher-volatility name is a more manageable way to express a view without letting one bad quarter impair your overall portfolio meaningfully.

A long-term mindset genuinely matters here more than in most sectors. AI technology, as an investment theme, has a multi-year time horizon. The investors most likely to capture the returns are those who can hold through the volatility cycles rather than being forced out of positions during downturns by having sized too aggressively.

The Honest Bottom Line

The AI investment opportunity is real. The leading companies are generating genuine revenues, and the technology's long-term potential is as significant as any technology shift since the internet. But the current point in the cycle — after extraordinary gains in 2024 and 2025, with some sector volatility in mid-2026 — means the obvious trades have already been made. The remaining opportunities require more careful navigation than "buy Nvidia and wait."

The most durable approach: understand which layer of the value chain you're investing in, size positions appropriately for the risk each layer carries, and resist the urge to pile into names with extreme valuations on the basis that AI will solve everything. The technology is transformational. The returns will be unevenly distributed. And the investors who do best will be the ones who thought clearly about structure, not just enthusiasm.